Stablecoins - just better payment rails?

The typical narrative is that stablecoins are the way for CBDC's to exert social controls by central governments.

CDBD's are a way for central governments to exert social controls.

But not all stablecoins have to be CBDC's, although the opportunity certainly is there.

The question should be, What are the risks and problems from CBDC's?

- Censorship (social control)

- Lack of Privacy (implied to get to censorship)

- Inflation (money printing)

Those are the top three that I see.

The first two aren't inherent in stablecoins.

But stablecoins pegged to the USD are.

Assume that, as long as political currencies are used as a unit of exchange, and the treasuries/bonds behind them are subject to monetary policy, that stablecoins inherit all the characteristics of traditional money.

Then does stablecoins just replicate traditional finance, but with nicer, cheaper rails?

This is the most bearish outcome.

To me, it's still not bad.

The fact that Visa sees the writing on the wall and wants to be involved/co-opt is a good sign. For sure, they will want to find a way to keep their profit margins while offering lower costs.

But are there second-order effects from cheaper rails (assuming that's all it offers, which I'm not sure it does).

The costs of marginal costs

The familiar up-charge from small stores and restaurants tells you there's a problem when using your credit card forces additional fees or higher minimums.

This small additional costs create friction.

And while most places have to accept credit cards and the associated fees, they shouldn't need to.

Those additional charges shouldn't be necessary.

The marginal cost of commercial transactions has room to drop.

To zero?

That seems unlikely: processing anything, however small, takes some kind of transaction cost.

But, as in the case of Bitcoin, a satoshi is one hundred-millionth of a Bitcoin.

So micro-fees for transactions that are accurately recorded and added to transactions could still support decentralized infrastructure while providing near-zero costs to spend or accept money, no matter what the size.

The common spaces for this solution would include global remittances, micro-payments in lieu of advertising, and easier-to-build alternatives to platform fees such as Apple's cut (this is only part of the problem since Apple's massive aggregation power still earns it a meaningful take rate.

Better rails from lower costs unleashes more economic activity.

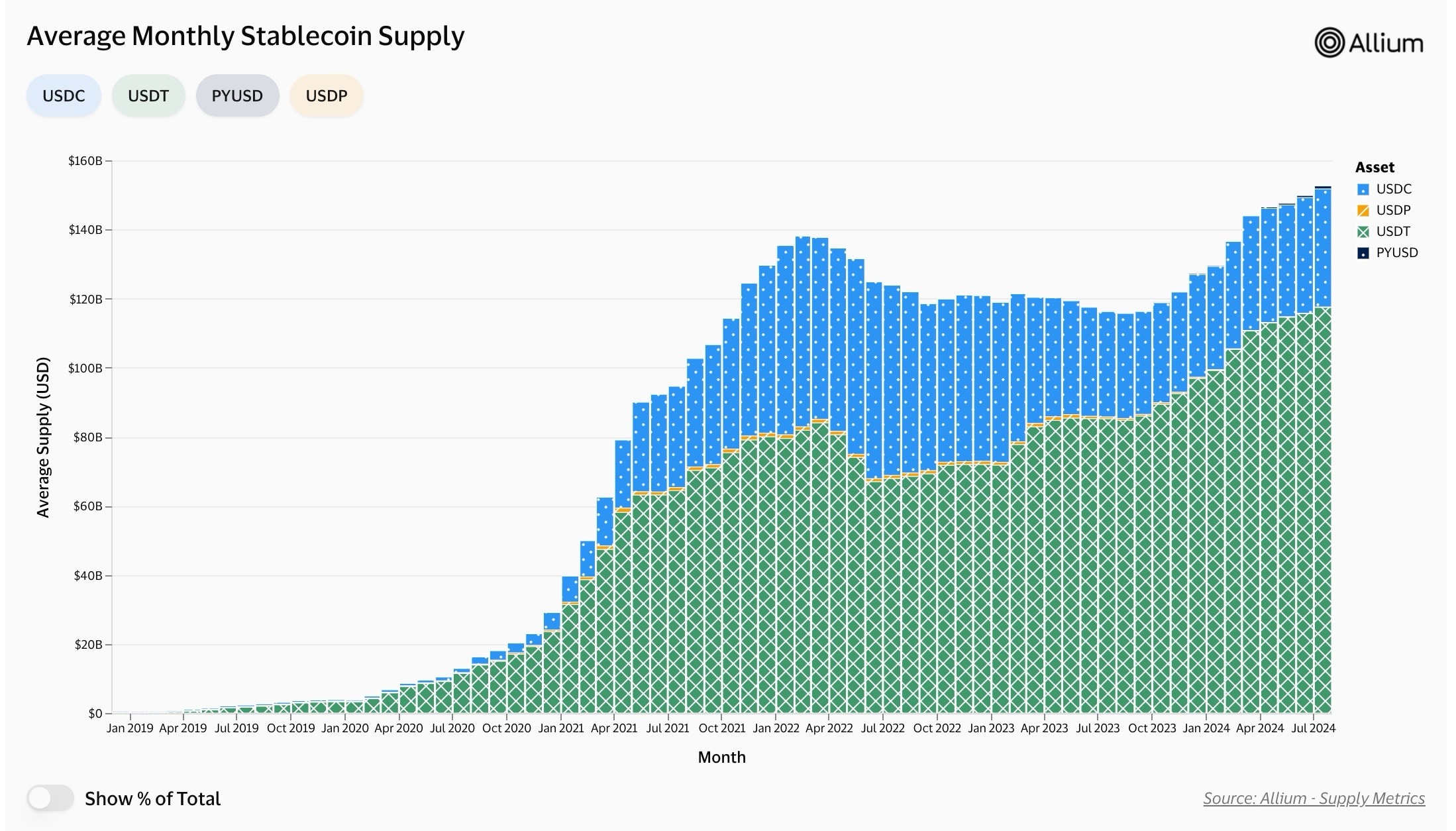

But in the case of USDC, it could also promote US dollar dominance.

Is this going to be good long term and will people still do it given the degree to which new money is injected into the system, debasing the value? For stable coins that may be backed by treasures or dollars, will there be a flight to stronger money?

There is that risk.

But all things are relative.

Enabling easy, friction-fee, conversions to USDC for people living in countries where their currencies debase much faster can be life-changing.

Savings in USDC, even if there were no native yield, preserves value when inflation is 70% a year.

The lower the friction, the more likely vendors want to accept USDC; which encourages more spending, which increases transactions in USDC versus a country's native currency.

Is a US dollar-pegged stablecoin (or coins) that dominates global commerce a good thing?

That depends on what you consider good.

Right now, with the decrease in sovereigns owning US Treasuries, anything which can increase the adoption helps the US government.

Countries with debasement that start to flip to USDC, on the other hand....could this actually be a trigger for more political instability due to crackdowns?

In general, freedom of anything along efficient rails is disruptive to some and freeing for others.

The Internet illustrates what happens when information was set free.

Twitter illustrates what happens when the public square is set free.

The Internet caused lock-downs, such as in China, because free information threatened their government.

Twitter enabled Arab Spring, but backlash resulted in tighter controls.

As computing costs went down and more portable, such as the smart phone, created new business models that weren't possible before.